Executive Summary

South Korea is emerging as one of the most important testbeds for Nvidia’s next phase of AI infrastructure.

The country is not merely a buyer of Nvidia hardware or a supplier of high-bandwidth memory. It is becoming a dense industrial environment where memory, telecom networks, cloud platforms, sovereign AI infrastructure, robotics, automotive systems, and advanced manufacturing can converge around the AI factory model.

That distinction matters.

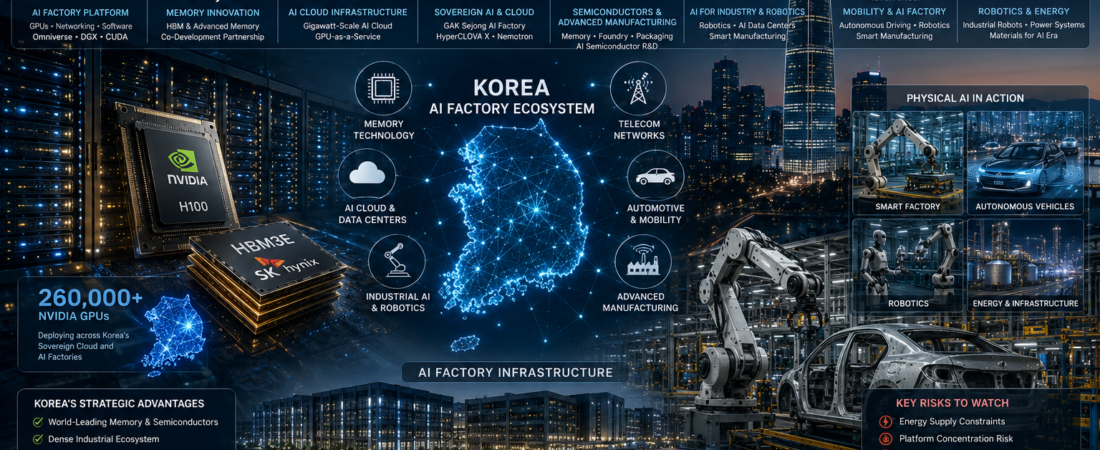

In 2025, Nvidia and South Korea announced plans to deploy more than 260,000 Nvidia GPUs across sovereign cloud infrastructure and private-sector AI factories. Since then, Nvidia’s Korea strategy has deepened through partnerships involving SK Hynix, SK Telecom, Naver, Hyundai Motor Group, LG, Doosan, and other industrial players.

Taken individually, these announcements resemble familiar AI infrastructure deals. Taken together, they point to something more structurally significant: Korea is becoming a national-scale laboratory for Nvidia’s AI factory concept — the idea that AI-optimized computing infrastructure will not only sit in data centers, but also become embedded in factories, vehicles, robots, telecom networks, and industrial operating systems.

For investors and strategists, Korea’s position in this transition should not be understood only through the lens of HBM supply. The larger question is whether Korea can turn its manufacturing base, cloud infrastructure, memory leadership, and industrial conglomerates into a full-stack AI production ecosystem.

Key Development

The foundation of Nvidia’s Korea engagement is memory.

SK Hynix and Nvidia have announced a multiyear technology partnership covering next-generation memory development for Nvidia’s AI infrastructure roadmap. The partnership includes memory technologies for future Nvidia platforms such as Vera Rubin AI systems and robotics-oriented computing platforms. SK Hynix is already one of Nvidia’s most important HBM suppliers, but the new arrangement moves the relationship closer to roadmap-level collaboration rather than simple procurement.

That matters because memory is no longer a supporting component in AI infrastructure. It is one of the main performance and cost bottlenecks. As AI systems scale, the interaction between GPU architecture, memory bandwidth, power consumption, packaging, and system design becomes increasingly important. A memory supplier involved earlier in the product roadmap gains strategic relevance beyond unit shipments.

The telecom and cloud layer adds another dimension. SK Telecom has moved toward building AI cloud infrastructure using Nvidia technology, while SK Group’s broader AI factory ambitions are tied to GPU-as-a-service, digital twins, semiconductor operations, and industrial AI applications. This creates a vertical stack inside one corporate group: memory through SK Hynix, telecom and cloud through SK Telecom, and manufacturing applications across the wider SK ecosystem.

Naver extends the story into sovereign AI and platform infrastructure. The company has announced plans to expand AI infrastructure from its GAK Sejong data center base toward gigawatt-scale AI factories using Nvidia’s infrastructure stack. Naver’s role is especially important because Korea’s AI ambitions cannot rely only on hardware. They also require domestic cloud platforms, Korean-language model development, enterprise AI adoption, and sovereign AI capacity.

The industrial layer is where Korea’s case becomes more distinctive. Hyundai Motor Group connects Nvidia’s AI factory strategy to automotive systems, robotics, autonomous driving, and manufacturing simulation. LG connects it to manufacturing, robotics, consumer electronics, data center technologies, and AI-enabled industrial operations. Doosan adds exposure to robotics, energy systems, industrial materials, and manufacturing applications.

This is why Korea matters to Nvidia. It is not just a market. It is a compact industrial ecosystem where Nvidia can test how AI infrastructure moves from data centers into the physical economy.

Strategic Analysis

Nvidia’s AI factory concept is a platform strategy, not just a hardware sale.

Nvidia’s use of the term AI factory reflects a broader strategic shift.

A traditional data center stores, processes, and serves digital workloads. An AI factory is designed to produce intelligence at scale. It combines GPUs, networking, memory, software frameworks, digital twins, model training, inference infrastructure, and industrial applications into a single operating model.

This is more than a product category. It is a platform strategy.

Once a company or country builds around Nvidia’s hardware, networking, CUDA ecosystem, Omniverse simulation tools, robotics platforms, and AI software stack, switching costs rise. The customer is not only buying chips. It is adopting an operating layer for future AI production.

Korea’s partnerships with Nvidia should therefore be read as anchor deployments of a platform across multiple industrial domains.

Korea’s industrial structure makes it unusually suited for this model.

Most national AI infrastructure projects focus on cloud capacity and data centers. Korea’s case is broader.

The country has leading memory producers, advanced manufacturing companies, telecom operators, internet platforms, robotics developers, automotive groups, electronics giants, and large industrial conglomerates. These capabilities are concentrated in a relatively small number of corporate groups that can coordinate large-scale deployment across multiple layers of the AI value chain.

That structure gives Korea an advantage as an AI factory testbed.

SK Group connects memory, telecom, cloud infrastructure, and industrial applications. Hyundai connects automotive systems, robotics, manufacturing, and mobility. LG connects electronics, robotics, data center technologies, and manufacturing operations. Naver connects cloud, sovereign AI, language models, and enterprise platforms.

In many countries, those layers would be spread across fragmented ecosystems. In Korea, they can be aligned more quickly through a small number of strategic corporate relationships.

The convergence of memory, cloud, and physical AI could create a flywheel.

If the announced partnerships develop as planned, Korea could occupy a distinctive position in Asia’s AI infrastructure map.

The potential flywheel is clear.

Advanced memory development supports Nvidia’s AI hardware roadmap. AI hardware deployments create demand for sovereign cloud and industrial AI infrastructure. Industrial AI deployments generate operational data from factories, vehicles, robots, logistics systems, and telecom networks. That data strengthens model development and simulation environments. Stronger models and simulation tools increase demand for more compute, more memory, and deeper platform integration.

This is the core of the Korea opportunity.

Korea does not need to become the largest AI data center market in Asia to matter. It needs to become one of the most advanced industrial AI deployment environments.

That would give the country a role that is different from Singapore’s data center position, Taiwan’s foundry position, Japan’s robotics and industrial automation base, or Southeast Asia’s power-and-land-driven data center buildout.

Platform concentration is the main strategic risk.

The same structure that makes Korea attractive also creates risk.

Korea’s AI infrastructure ambitions are increasingly tied to Nvidia’s hardware and software ecosystem. That concentration may deliver speed, performance, and global relevance, but it also creates dependency.

Nvidia gains leverage when its GPUs, networking systems, software frameworks, robotics tools, and digital twin platforms become embedded in national infrastructure. Korean companies may benefit from early access and deep integration, but they may also face future pricing power, roadmap dependency, supply constraints, and limited bargaining flexibility.

Samsung’s role is especially important to watch. It remains a central player in Korea’s semiconductor ecosystem through memory, foundry, advanced packaging, and electronics manufacturing. Its position in HBM qualification, foundry competitiveness, and AI factory deployment will shape whether Korea’s Nvidia-centered ecosystem remains balanced or becomes more heavily tilted toward specific corporate groups.

Energy and infrastructure constraints remain unresolved.

AI factories require enormous amounts of power.

Gigawatt-scale AI infrastructure is not only a semiconductor problem. It is also a grid, cooling, land, permitting, and energy procurement problem. Korea’s industrial density gives it advantages in deployment coordination, but the country still faces power constraints, land limitations, and grid-planning challenges.

This matters because AI infrastructure plans are often announced in GPU counts, but executed through substations, power purchase agreements, cooling systems, and regulatory approvals.

If Korea cannot expand reliable power supply and data center infrastructure fast enough, its AI factory ambitions may face the same bottleneck now visible across Southeast Asia and other AI infrastructure markets.

Investor Takeaway

The SK Hynix–Nvidia memory roadmap partnership is the most strategically significant layer. Co-development at the memory architecture level embeds SK Hynix deeper into Nvidia’s future AI infrastructure roadmap. Investors should watch how this relationship evolves alongside Samsung’s HBM progress and the broader shift toward memory as a system-level bottleneck.

Naver deserves more attention as a sovereign AI infrastructure player. Naver’s AI factory and cloud ambitions connect Korea’s hardware strength to domestic platform capacity. Its ability to scale infrastructure, serve enterprises, and support Korean-language AI development will determine whether Korea can build more than a hardware-dependent AI strategy.

Physical AI is the long-term upside. Hyundai, LG, Doosan, and other Korean industrial groups give Nvidia real operating environments in which to test robotics, automotive AI, smart manufacturing, digital twins, and industrial automation. These applications may take years to monetize fully, but the operational learning could become strategically valuable.

Platform concentration is the core risk. Korea’s Nvidia alignment accelerates its AI infrastructure buildout, but it also increases dependency on a single dominant technology stack. Future diversification through domestic AI chips, alternative accelerators, sovereign software layers, or multi-vendor infrastructure will be an important signal.

Korea’s AI factory strategy should be judged by deployment, not announcement volume. The most important indicators will be power availability, data center construction progress, enterprise adoption, HBM roadmap execution, cloud utilization, and real industrial AI use cases. GPU commitments are only the starting point. The strategic question is whether Korea can turn that compute into durable industrial advantage.